Line 6 - Social Security and Railroad Retirement Benefits

- Up to 85% of Social Security benefits may be taxed on the federal return.

- Computationally, if AGI plus any tax-exempt income plus one-half of Social Security benefits is less than $25,000 ($32,000 for MFJ), none of the Social Security benefits will be subject to tax. Nevertheless, all potentially taxable Social Security benefits must be entered in TaxSlayer.

- Social Security benefits (on Form SSA-1099), and Railroad tier 1 benefits (on Form RRB-1099; see “blue form” below), are treated similarly on the federal return. Unless otherwise specified, the term “Social Security benefits” in this section refers to both.

- Social Security Disability Insurance (SSDI) benefits are treated, for tax purposes, as regular Social Security benefits. A Form SSA-1099 is issued for SSDI.

- Taxpayers can get a copy of a missing SSA-1099 from their local Social Security office or by calling 800-772-1213.

- Other benefits paid by the Social Security Administration are treated differently:

- Benefits received by a child of a deceased taxpayer are NOT taxable on a parent’s or guardian's return, but must be entered on the child's return if the child has a filing requirement.

- Social Security death benefits (maximum $255) paid to the deceased’s spouse or children are NOT taxable.

- Supplemental Security Income (SSI) benefits are NOT taxable; no SSA-1099 should be issued.

- Enter Social Security benefits received by the taxpayer during the tax year on the Social Security SSA-1099/RRB-1099 Tier I page [Income > Form 1099-R / RRB, SSA > Social Security Benefits/RRB-1099].

- Information for both taxpayer and spouse are entered on the same page.

- Enter the amount in box 5 of SSA-1099 and box 5 of RRB-1099 (blue form) on the line “Taxpayer's Social Security Benefit.”

- If there is more than one paper form for a person for the same year, combine amounts on all paper forms to see if the amount is positive or negative. If positive (which is normal), enter the total; if negative, see below.

- A typical situation where a taxpayer has two SSA-1099s is when the taxpayer got Social Security benefits based on his or her own earnings for part of the year, and got benefits based on spousal or survivor earnings for the other part of the year. In such case, box 8 won’t be the same on the two forms.

- TaxSlayer automatically calculates any taxable amount, on Form 1040 Line 6b.

- No form provided by the taxpayer: The Social Security Administration does not issue an SSA-1099 form for a taxpayer whose SS benefits are less than the Medicare premiums (typically just Part B) that are being paid from SS benefits. More commonly, a taxpayer has misplaced or perhaps not received the form in the mail. There are alternatives to asking the taxpayer to go to the nearest SSA office to get a copy:

- Taxpayers sometimes bring a letter from the SSA that states what they’ll receive in the upcoming year.

- Use the amount on last year’s tax return (or last year’s SSA-1099) together with the standard cost-of-living increase.

- For calendar year 2025, SSA benefits increased 2.5% compared to 2024; the increase was 3.2% for 2024, 8.7% for 2023; 5.9% for 2022; and 1.3% for 2021 compared to 2020.

- Negative amount: If the amount in box 5 of a paper form is negative, it can be offset by a positive amount on another SSA-1099 received by the taxpayer – enter the net amount. On a MFJ return, if the total amount for one person is negative, enter a zero for that person and reduce the amount of the other person appropriately. If the 1099-SSA cannot be fully offset, the next step depends on the amount:

- If the amount is $3,000 or less, do nothing. It would’ve been subject to the obsolete federal 2%-of-AGI reduction (deductions suspended through 2025). And since Social Security benefits are never taxed by California, the amount isn’t relevant to the CA return.

- If the amount is over $3,000, the amount is not subject to the 2%-of-AGI reduction and can be entered in the federal return in one of two ways.

- As an itemized deduction. On the Schedule A - Miscellaneous Deductions page, enter the amount in the “Repayment under claim of right” box.

- Note for CA returns: Repayments of any SS benefits are not deductible as a CA itemized deduction because the original payment was not taxed by CA (A). An adjustment (reduction of itemized deductions) is needed on CA Schedule CA Part II line 21. On the “Itemized Deductions” page of the CA State Section, enter the amount in the “Subtractions - Other Miscellaneous Itemized Deductions” box.

- As a credit (out-of-scope). The credit amount is entered on the IRC 1341 Repayment Amount page [Federal > Payments & Estimates], and appears on Schedule 3 Line 13z, with the notation “IRC 1341”.

- Calculating the amount of this credit may be difficult or impossible if it spans multiple years. If it involves only one year, the credit is essentially the taxable amount times the marginal tax rate.

- If it seems the taxpayer would benefit significantly from taking this credit, rather than an itemized deduction, they should see a full-time paid preparer.

- Enter any federal tax withheld (box 6 of SSA-1099, box 10 of RRB-1099) on the appropriate line.

- Take care not to enter Medicare payments on the line for federal tax withheld. (Few taxpayers have taxes withheld from Social Security benefits, so this line is normally left blank.)

- Medicare premiums listed on the SSA-1099 or Form RRB-1099 should be entered in one of two places:

- If the tax return has self-employment income, enter Medicare premiums paid on Schedule C in TaxSlayer, as discussed on page 68; they might become a SEHI adjustment on Schedule 1.

- Otherwise, enter Medicare premiums on the Social Security SSA-1099/RRB-1099 Tier I page.

- Medicare premiums entered on Social Security SSA-1099/RRB-1099 Tier I page automatically flow to Schedule A medical costs. Do not reenter on Schedule A.

- If a paper form lists more than one Medicare premium, and premiums are not being entered in Schedule C, then total all premiums and enter in TaxSlayer.

- When there are multiple premiums on a paper Form SSA-1099, it’s helpful to mark what dollar amounts were totaled, and write the total on the paper Form SSA-1099 for the quality reviewer.

- Attorney fees listed on a Form SSA-1099 don’t affect either federal or CA return.

- Note for CA returns: Neither Social Security benefits nor Railroad tier 1 benefits are taxed by California (B). TaxSlayer makes the adjustment automatically on CA Schedule CA Part I, Section A line 6.

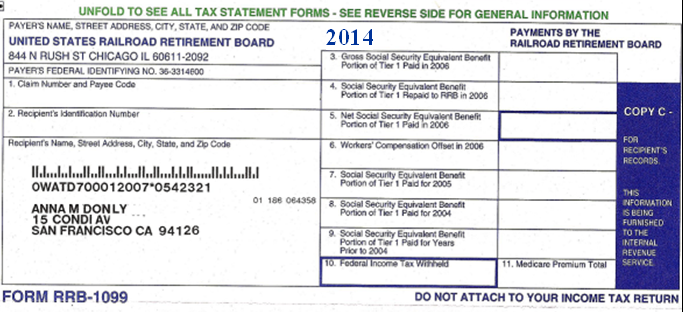

RRB-1099 – Blue Form/“Tier 1 Social Security equivalent”

|

Amounts on the RRB-1099 |

Enter in TaxSlayer on Social Security SSA-1099 page |

|

Box 5 |

Equivalent to Social Security payments, for taxpayer or spouse |

|

Box 10 |

Federal tax withheld for taxpayer or spouse |

|

Box 11 |

Medicare total for taxpayer or spouse; TaxSlayer carries to Schedule A |

Lump Sum Payments of Social Security

- When some of the current-year Social Security payments are attributable to a prior year(s), that is stated in the “DESCRIPTION OF AMOUNT IN BOX 3” on Form SSA-1099. In this case, TaxSlayer can do an alternate calculation of the amount that is taxable on the federal return, potentially benefiting the taxpayer.

- Total Social Security payments received (box 5 of the SSA-1099) is entered as usual; do not change the entry in TaxSlayer because of lump sum payments.

- If, after all income in the Federal Section has been entered, Line 6b or 15 on Form 1040 is zero, STOP – it is not necessary to complete the lump-sum payment worksheet in TaxSlayer.

- If the taxpayer does not have any of the tax returns for the prior year(s) for which the retroactive Social Security benefits were received, it’s not possible to complete the lump-sum payment worksheet in TaxSlayer, which is required for the alternative calculation.

- The taxpayer’s options are (1) request a [free] transcript from IRS for the missing year(s) (Form 4506-T] , or (2) treat the retroactive benefits for the missing year(s) as received in the current tax year (don’t do the alternate calculation). Note: There is a fee to get a photocopy of a filed return.

- If the taxpayer has only some of the tax returns for the prior year(s) for which retroactive Social Security benefits were received, then complete the lump-sum payment worksheet in TaxSlayer for those year(s). Even one year can help!

- If Line 6b on Form 1040 is not zero, AND information from any of the prior year return(s) is/are available:

- On the Social Security SSA-1099 page, click “Begin Worksheet”, and follow the instructions on NTTC 4012 page D-69 for each prior year.

- The TaxSlayer print package contains the worksheets for all years.

- If the taxpayer is eligible for Premium Tax Credits (page 93), the entire lump sum is part of the taxpayer’s MAGI, regardless of whether the lump sum method is used to determine the tax.

Canadian or German Social Security

- For U.S. taxpayers, Canadian or German Social Security income is treated the same as U.S. Social Security.

- Canada’s versions are the Canada Pension Plan (CPP), Quebec Pension Plan (QPP), and Old Age Security (OAS).

- Follow instructions on NTTC 4012 page D-70 to convert to U.S. dollars and enter in TaxSlayer.

- Note for CA returns: Canadian and German social security payments are taxable for California. (A)

- TaxSlayer does not make the correct adjustment for CA – it treats Canadian and German social security payments as if they were U.S. Social Security payments.

- Enter the adjustment amount – the entire amount of the Canadian and German social security payments - as an addition to CA income, as described in the section Manually Entering Income Differences on CA Schedule CA, page 102.

Created with the Personal Edition of HelpNDoc: Elevate Your CHM Help Files with HelpNDoc's Advanced Customization Options